Week 4, Spring ER Season 2022

Variable results in a choppy market

I am a systems trader that needs to have rules in place that help me eliminate all reasons to NOT take a trade before I actually enter a trade. Within these systems, probability based on past performance of various setups leading up to and during earnings releases of equities plays a very important role in determining what I plan for the following week.

If you live in Florida and want to buy hurricane insurance in December, the premium for that policy will be low. However, the premium will go up in May going into hurricane season. It will shoot up even higher if you try to buy a policy when a hurricane is 50 miles away and making a beeline towards your city. As soon as the storm passes, hopefully missing you, a new policy’s premium shoots down as the probability of causing damage disappears.

Options, whose premiums are heavily influenced by implied volatility, are like insurance policies. If implied volatility goes up, so do option premiums; if it goes down, so do option premiums. Fluctuation of implied volatility is caused by a known event, earnings releases, that causes higher probability of “damage” (unexpected price rise or fall). Behaviour of implied volatility leading up to, during, and following earnings is one of the most predictable elements in the market.

Some equities exhibit patterns of having consistently high implied volatility just before earnings are announced, volatility crush in the day following earnings combined with low price movement. These patterns are ideal set ups for a very short term (24 hour) iron condors.

Each Sunday evening, our Swing Trading / ER Strategies group at optionsplayers.com sorts and identifies key equity targets based on a success rate of 75% or greater over the past four earnings releases for an iron condor strategy and develops a play book of rules for the upcoming week. The following is a post mortem review of our previous weeks candidates:

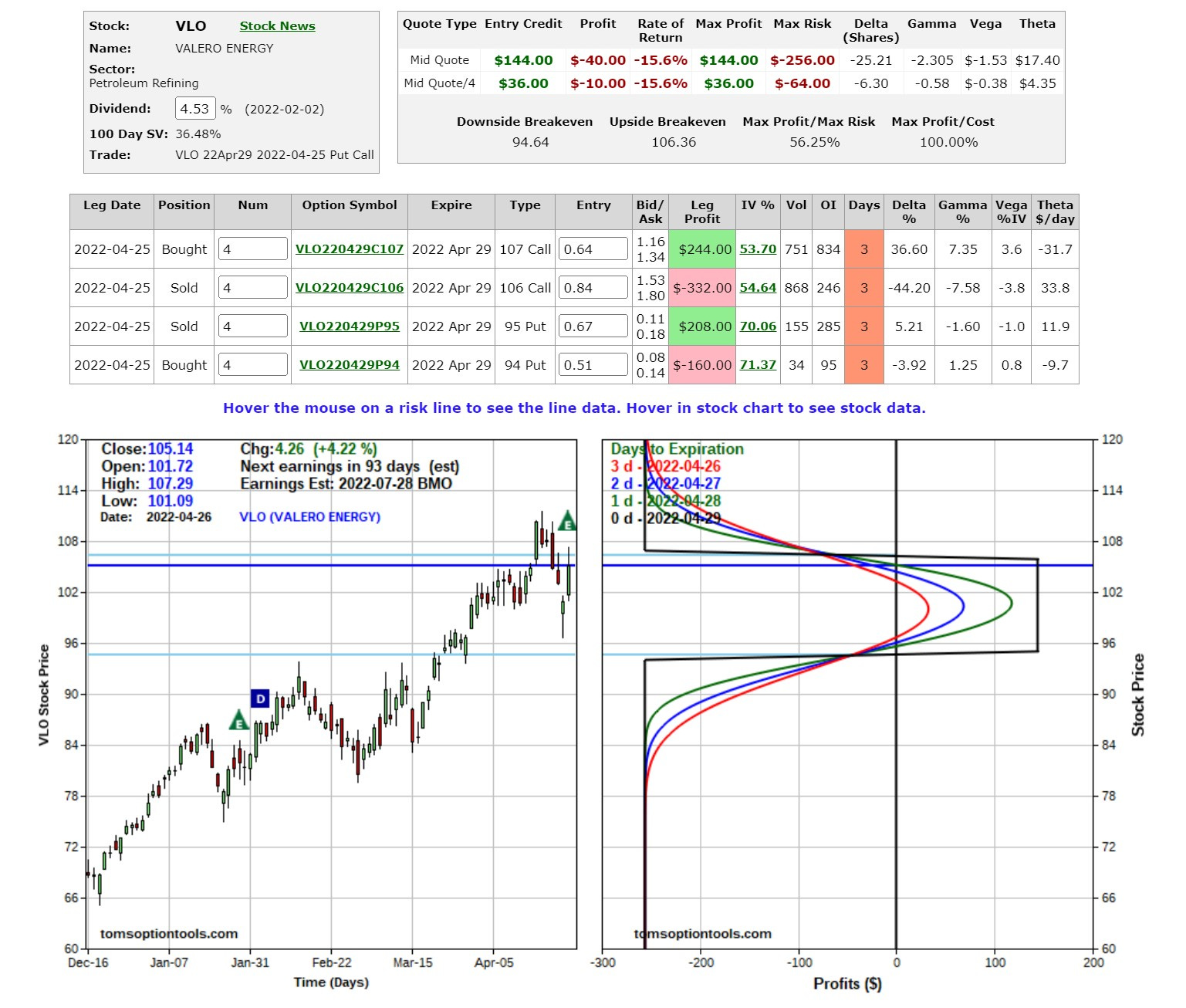

VLO

VLO usually reports before market open. IV crushes overnight from the close the day before through the end of the day of the earnings report. Over the past four earnings releases, the average price move for VLO was 1.28%. Entering an iron condor at close the day before and exiting the day of earnings had a win/loss ratio of 100%.

I entered a four VLO Apr29 $94/95/106/107 iron condor on Monday, April 25th at 15:43 for $0.36 (0.64 risk) each for a total risk of $256.

Unfortunately, VLO moved 4.22% to close at $105.14 and implied volatility did not drop as would be normally expected. The trade was exited for a 15.6% loss ($40) at he end of the day on Tuesday April 26th.

MMM

MMM usually reports before market open. IV crushes overnight from the close the day before through the end of the day of the earnings report. Over the past four earnings releases, the average price move for MMM was less than 3%. Entering an iron condor at close the day before and exiting the day of earnings had a win/loss ratio of 100%.

I entered a one MMM Apr29 $136/141/155/160 iron condor on Monday, April 25th at 15:47 for $1.30 (3.70 risk) each for a total risk of $370.

MMM moved 2.95% and closed at $144.22, well above the short $141 put strike. Implied volatility crushed. I was able to buy back the position for $0.60 thirty minutes before close on Tuesday, resulting in a $70 profit (16.21% ROI).

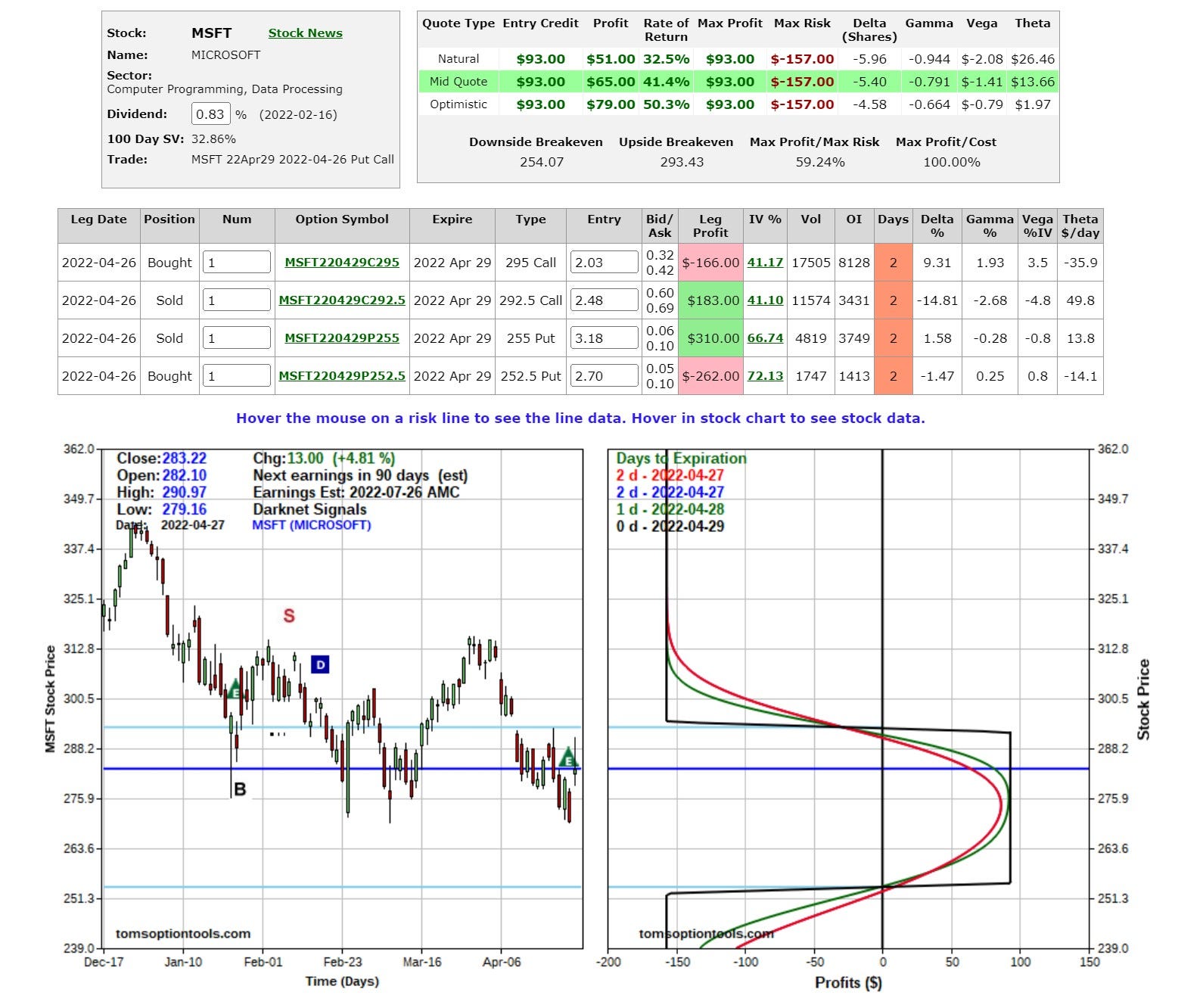

MSFT

MSFT usually reports after market close. IV crushes overnight from the close the day of earnings through the end of the following day. Over the past four earnings releases, the average price move for MSFT was less than 5%. However, the corresponding IV crush more than offsets the move in price. Entering an iron condor at close the day of and exiting the day after earnings had a win/loss ratio of 75% over the past year.

I entered a one MSFT Apr29 $252.50/255/292.50/295 iron condor on Tuesday, April 26th at 15:41 for $0.93 (1.57 risk) each for a total risk of $157.

MSFT moved 4.81%% and closed at $283.22, well below the short $192.50 call strike. Implied volatility crushed. I was able to buy back the position for $0.29 ten minutes before close on Wednesday, resulting in a $64 profit (40.67% ROI).

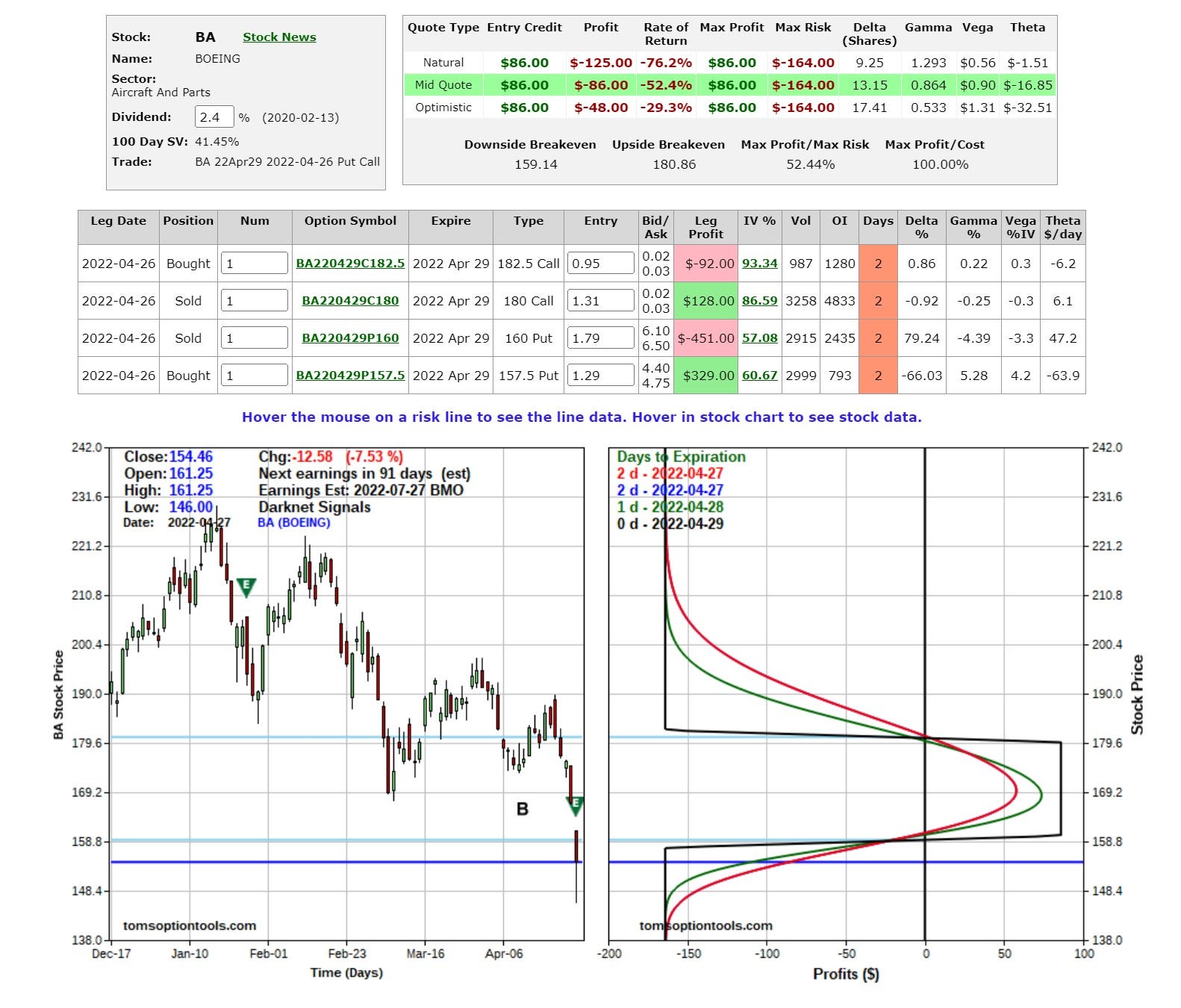

BA

BA usually reports before market open. IV crushes overnight from the close the day before earnings through the end of the following day. Over the past four earnings releases, the average price move for BA was 4.56%. However, the corresponding IV crush normally more than offsets the move in price. Entering an iron condor at close the day before and exiting the day of earnings had a win/loss ratio of 75% over the past year.

I entered a one BA Apr29 $157.50/160/180/182.50 iron condor on Tuesday, April 26th at 15:45 for $0.86 (1.64 risk) each for a total risk of $164.

BA moved 7.53% and closed at $154.46, beyond the two put strikes. I was able to buy back the position for $1.70 near close, resulting in a $84 loss (-51.2% ROI).

GILD

I had two separate trades on GILD, one directional and one non-directional over earnings. It was identified on Sunday evening, April 24th to be in an upward trend with the probability of implied volatility rush leading up to earnings on Thursday during a live stream for the Optionsplayers.com Swing Trading / ER Strategies group.

Four GILD Apr29 $62.50 calls were bought for $1.00 each (total debit $400) with a plan to close the position just before earnings on Thursday. GILD did not perform well, however the implied volatility increase helped prop up the value. The position was sold per plan for $0.65 per contract for a total loss of $140 (-35% ROI)

The second trade was based on a historical pattern of implied volatility crush combined with low price movement post earnings in the same manner as the other non-directional trades over the week.

I entered four contracts of a GILD Apr29 $58/59/64/65 iron condor on Thursday, April 28th at 15:45 for $0.28 ($0.72 risk) each for a total risk of $288.

GILD moved 3.61% and closed between the short strikes. The position expired worthless resulting in a $112 gain (38.89% ROI).

OTHER

Four other opportunities were identified at the beginning of the week on FSLR, LLY, and MA. No positions were entered due to violation of liquidity rules on their options.

2 - 6 MAY PLANNED IRON CONDORS

A list of candidates with 75% win/loss ratio over the past four earnings releases has been sent to the private Swing Trading / ER Strategies group (fee paid) and will be discussed in a live stream on Sunday evening, May 1st.

PERFORMANCE TO DATE