JPM Earnings Play

Here is this Earnings Season’s first play:

Over the past four ER’s, JPM has moved 4.24%, 3.49%, 2.52%, and 1.66% for an average move of 2.98%.

The standard Green Goose Earnings play is to sell an Iron Condor just before the earnings call (at close the day before if reporting before market open or at close the day of if reporting after market close) with the short legs at +/- the cost of an at the money weekly straddle from the probable closing price. The long legs are placed one strike outside of the short strikes.

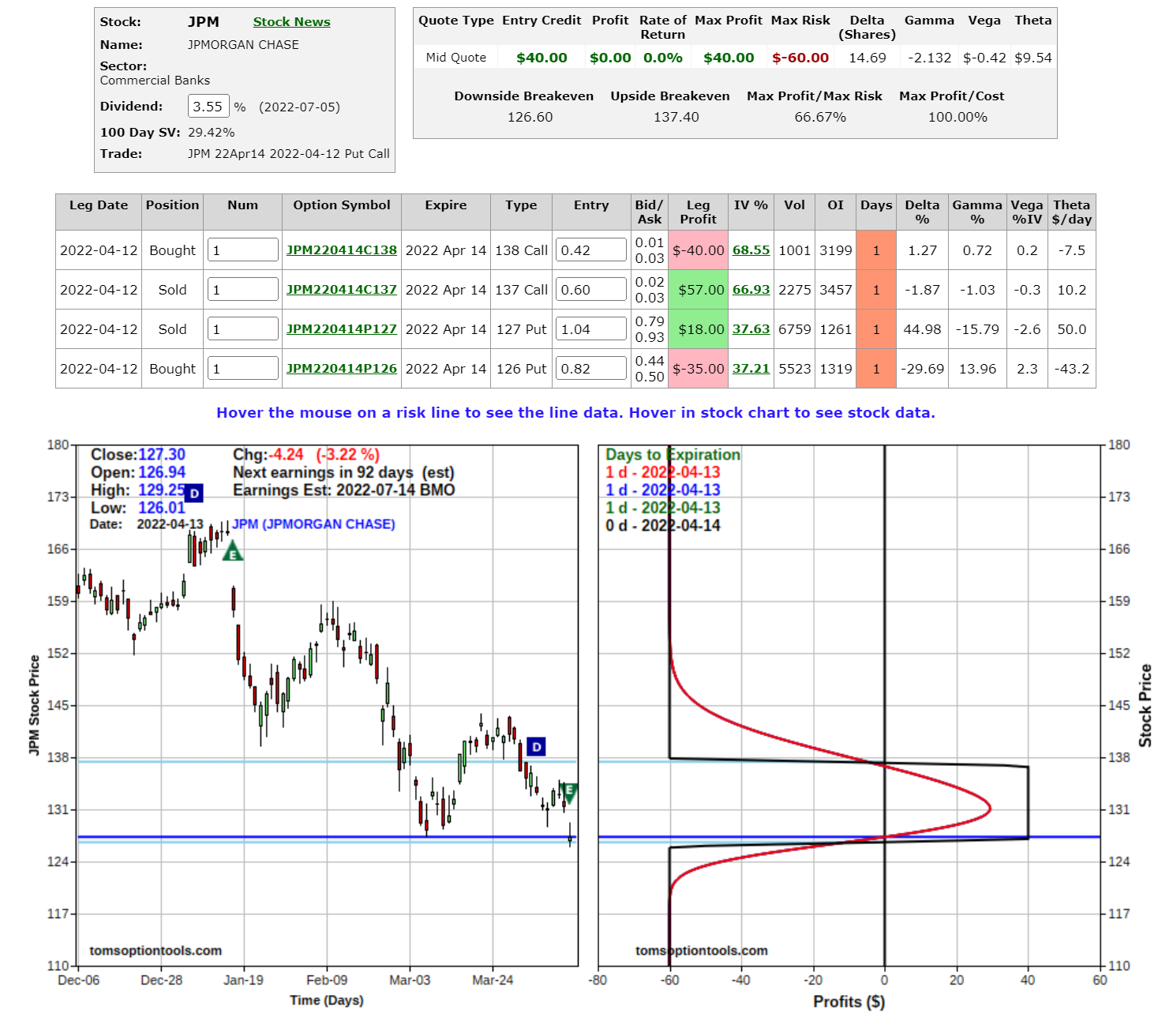

JPM (which reports before market open), on Tuesday, April 12th last year closed at $131.54 and an at the money $132 straddle (call + put) expiring on Friday, April 14th cost was $5.15. Therefore the ideal short strikes were $127 ($132-$5) and $137 ($132+$5). The long strikes were $126 and $138. Total premium available was $0.40 on $0.60 risk.

As stated many, many times, I like to size my iron condors over earnings releases with no more than $250. Therefore the above is position sized with 4 contracts for a total risk of $240. Potential earnings was $120.

The theory behind this type of earnings play is that Implied Volatility (IV) crushes and the underlying stock doesn’t move outside of the short wings, allowing the trader to buy back the iron condor for less than they received (for a profit). In the JPM example from one year ago, IV crushed, but the underlying stock moved to the break even - still a success…

Courtesy of Toms Option Tools.

The historical performance of JPM earnings iron condors over the past four ER’s is as follows:

April 12, 2022: 0%

July 14, 2022: -1.6%

October 14, 2022: +69.6%

January 13, 2023: +50.0%

While the above performance is “ideal”, the track record fits my criteria to play this time around.

I plan on selling a JPM Apr14 earnings iron condor in the last 15 minutes of open today (Thursday, April 13th). Exit will be EOD on Friday, hopefully with a worthless expiry.

If you decide to play, please do your own due diligence!!