Anatomy of a 24 hour Earnings Play with Options

Anatomy of a 24 hour Earnings Play with Options

A Case Study on NKE

Over the years, I have traded many types of setups and strategies. It is absolutely thrilling to see some of my favorite patterns unfold. Bull pullbacks/bear rallies, triangles, and head & shoulders/quasimodo’s jump out at me like a Banksy on a wall. The corresponding option strategies become integral parts of the puzzle. Straight calls/puts, debit & credit spreads, directional butterflies & calendars, risk reversals, Tarzan loves Jane’s and other exotic strategies all have their place in my toolbox. However, my most successful and consistent strategy has very little relationship with price action patterns on charts and centers around the behavior of implied volatility around earnings releases.

From Investopedia.com, Implied volatility (IV) is the market's forecast of a likely movement in a security's price. IV is often used to price options contracts where high implied volatility results in options with higher premiums and vice versa. Supply and demand and time value are major determining factors for calculating implied volatility.

What does this actually mean?

Market makers price option contracts higher when there is increased uncertainty of a potential price move in the underlying equity, albeit an individual stock or index or ETF. The last two months has seen a much higher fluctuation of asset price fluctuation so implied volatility has been higher than normal. The VIX is a window on the overall markets implied volatility.

Implied Volatility can be seen as a measure of supply and demand of options. While supply of option contracts is theoretically unlimited (market makers are there to provide liquidity), demand for those contracts rises due to uncertainty. It their core, options are insurance against adverse price movement of an underlying equity. Puts insure long stock positions against outsized moves down; Calls insure short positions against outsized moves up. Essentially, option prices rise as demand goes up.

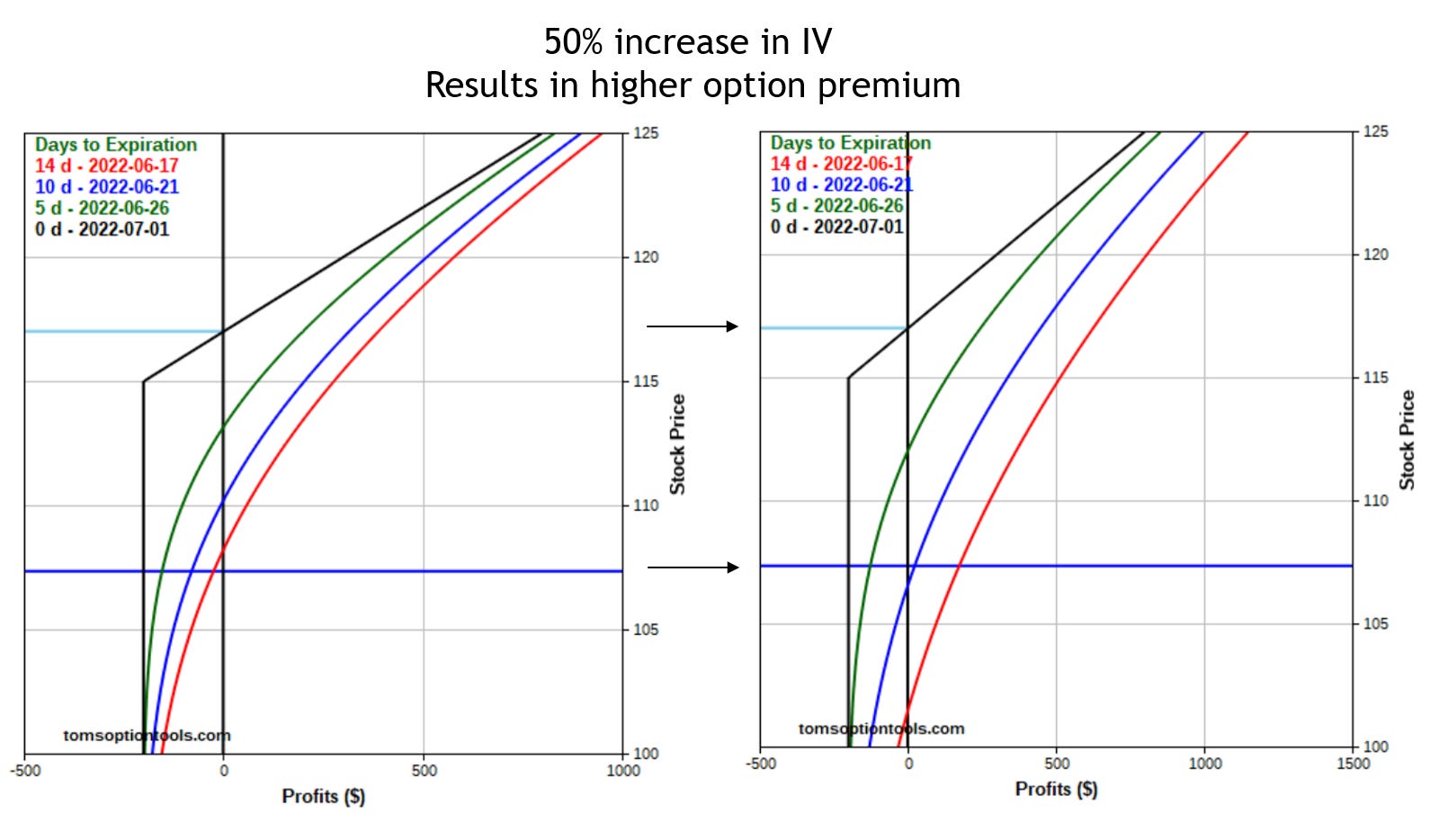

When implied volatility increases (rush), option premiums are juiced upwards; when it decreases (crush), option premiums decrease.

Is Implied Volatility something that is predictable? Yes and no…

No – for unplanned events. Well, they are unknown right!?

Yes – for certain situations, e.g., known events that cause uncertainty. Example Earnings Releases or major economic announcements.

Implied Volatility almost always “rushes” leading up to and “crushes” immediately following earnings reports. The run up in option premium prior to earnings reduces risk for the market maker who sold those options if the underlying stock makes a major move. The market maker profits if the stock makes a smaller move than the juiced up premium of those options “implies” and is either able to buy back the contracts for a lower price than they sold them or allow them to expire worthless.

As retail traders, how can we profit from this phenomenon?

Become the market maker!!! But not with unlimited risk… Introducing the 24 hour Market Maker (Earnings) Iron Condor…

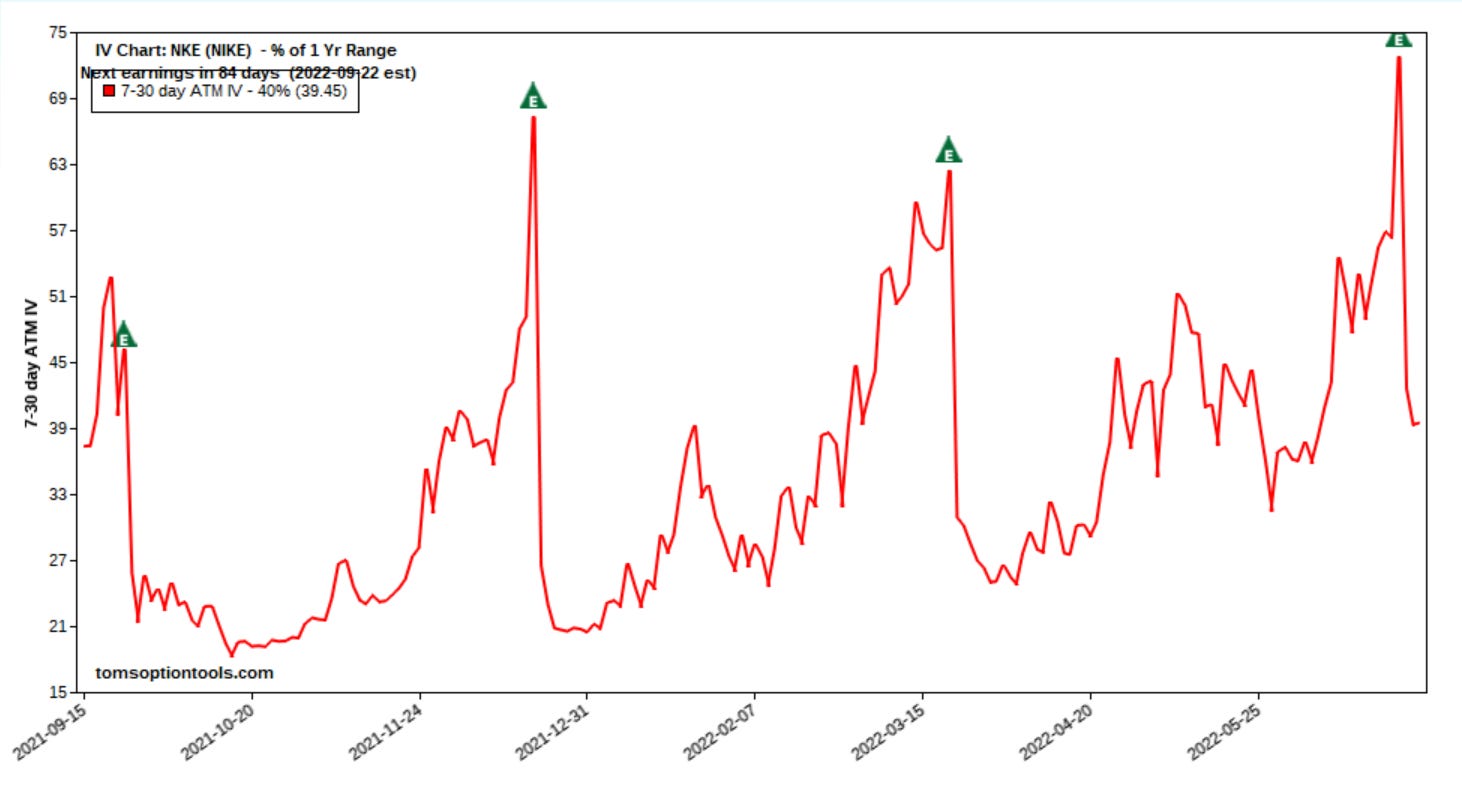

I have developed a tracking system over the years for roughly 120 different equities that have outsized IV rush heading into earnings, experience reversion to the mean IV crush, AND most important – have historically had price movements the day following ER that do not offset their options IV crush. This is my “secret sauce” and consistently generates a high win/loss ratio as well as above average profit factor when I sell a weekly iron condor 1 to 15 minutes before ER and exit/let expire 24 hours later. Depending on historical performance, I will play between 25 and 30 of those of the 120 that make the “go” list per ER season.

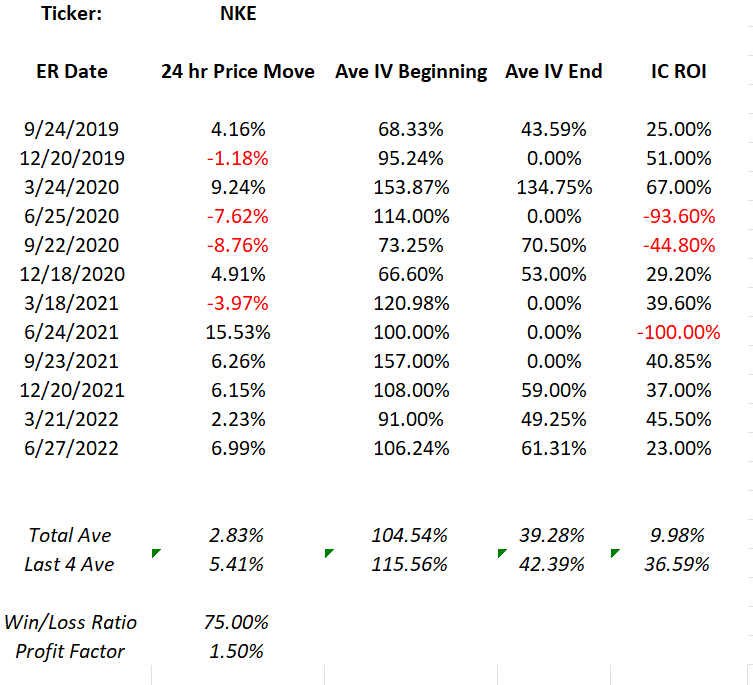

For example, NKE was the last play on my list for Spring 2022 ER Season (results from this past week are included):

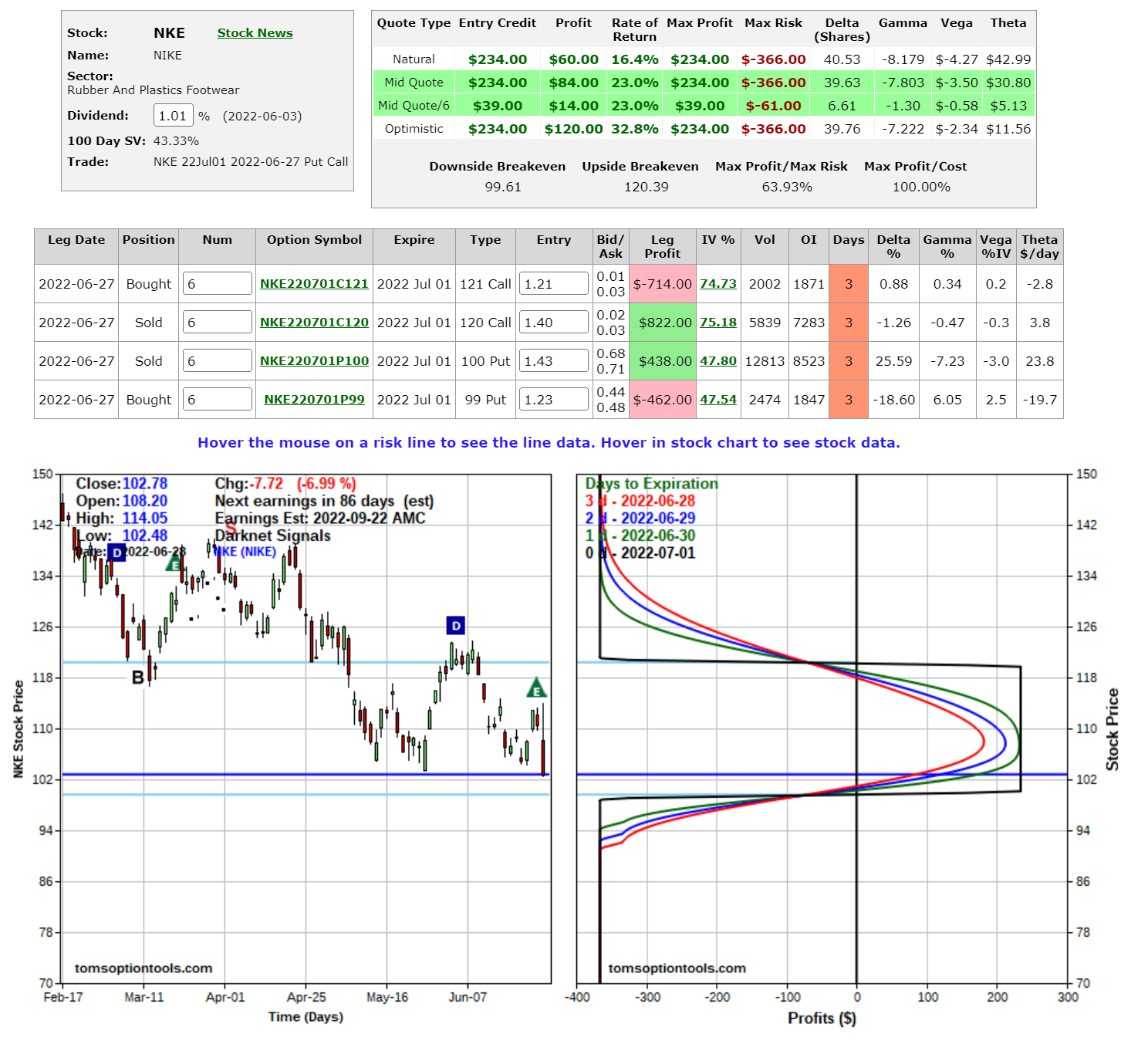

A NKE Jul01 $99/100/120/121 iron condor was alerted to the premium members of Green Goose Trader and entered just before market close on June 27th for $0.39 per contract ($0.61 risk).

The premium members were alerted at 15:00:00 on June 28th that I was exiting the iron condor by buying it back for $0.08 ($0.31 profit on $0.61 risk). Note that the pricing at 16:00 was less per below. IV crush offset the price move of NKE and profit was locked in.

Going forward, Green Goose Trader’s value is that the background research for similar ER plays has been done. Each Sunday during Summer 2022 ER season beginning in mid-July, as well as subsequent ER seasons, a list of validated ER plays will be presented for the coming week to premium subscribers. Additional pre-ER IV rush candidates will be identified and trade plans written during a Live Stream/recorded Market Review and Opportunity Discovery session or a written post. All opportunities will be actionable. (Free subscribers will gain access to the previous weeks recordings or written posts on the following Friday after market close when all plays have been completed.)

The first ER plays begin the week of July 11th.

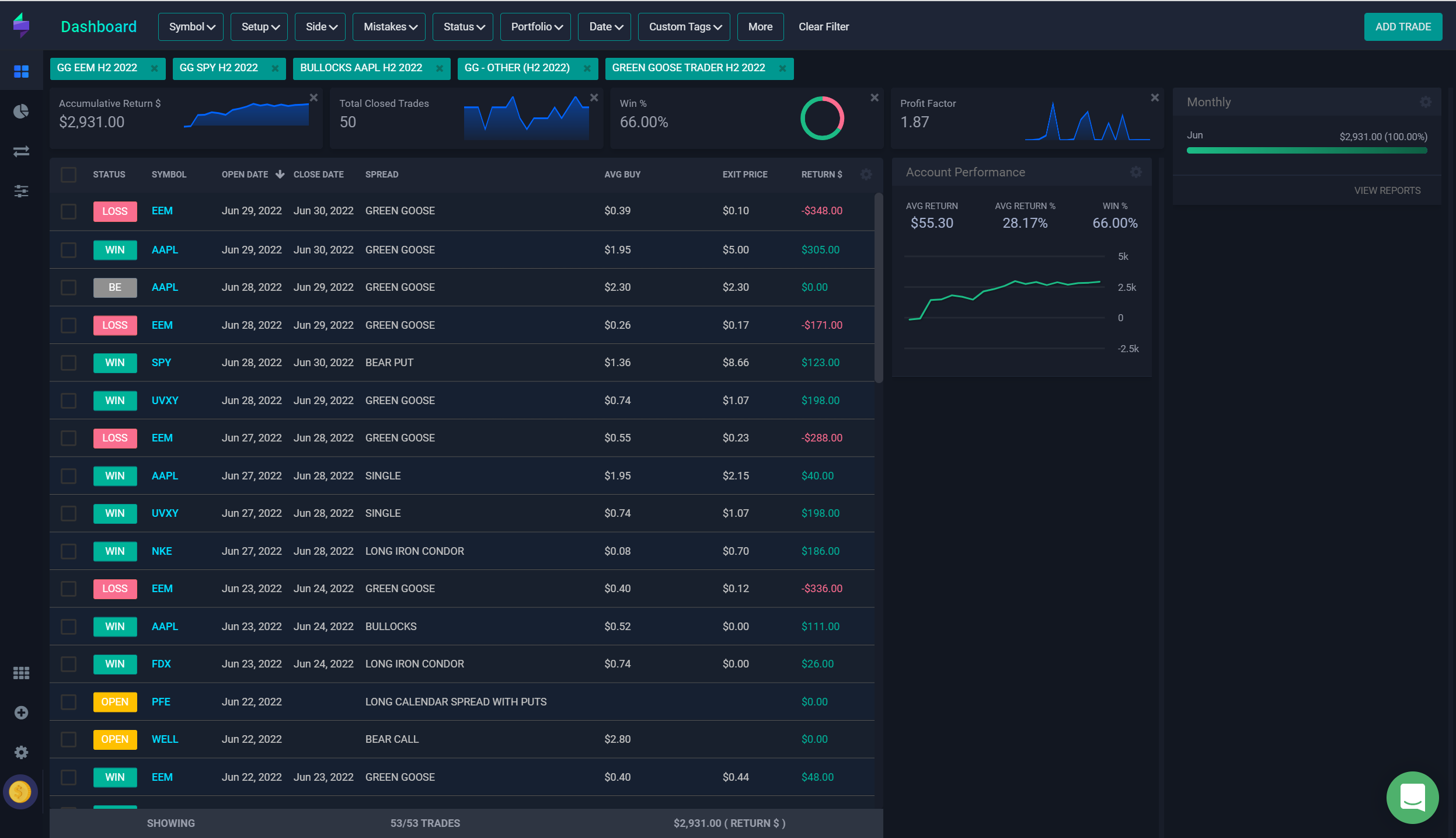

Results of all alerts (both closed and open plays are noted) for the month of June for GG Alerts and Green Goose Trader are as follows:

There are currently three open trades, a sideways play on PFE expiring on July 15th, a short play on WELL expiring on July 15th , and a short play on FEZ, expiring in August 19th. Each uses a position size (risk) of <= $250.

Note - I rely on both TraderSync and Toms Trading Room in my trading. They are the basis of my “edge.” I wouldn’t recommend them if I didn’t use them. Links are provided below for your convenience… Finally, membership in a community of like minded traders is a positive benefit if it helps you stay honest with yourself. There are many out there, one of which is optionsplayers.com.

FYI - Premium subscribers were alerted on Tuesday that I was exiting the FEZ play for $100 profit.